In the early morning of a Sunday in June last year, I had a very serious tummy ache. The ache was as if you wanted to let out a tons of waste (Shit) and your stomach cramps, however nothing came out. The symptoms became worse where my tummy seems to reject anything I put down the throat, even simple water, everything was sent out puking.

This episode of acute appendicitis got me thinking of covering the topic of hospitalization insurance plans in Singapore as I wasn’t prepared or fully understood my insurance entitlements be it personal or company. Looking back, if I had taken the time to read up my entitlements, it would have saved me from having the anxiety of potentially receiving a financial bomb.

Getting Hospitalized

My MediShield life integrated plan is insured by Aviva as there was a promotion where kids get free coverage when both parents are insured. For optimal premium, I opted for a private package with a high excess / 10% co pay level to optimize my cash premium with hindsight that’s so silly of me.

Morning of the incident, I went to a private hospital’s A&E for quicker response time. The doctors attended to me relatively fast, diagnosis was quick and a CT scan was requested to verify if it’s an acute appendicitis. Upon confirmation, the general surgeon explained the procedure, said it’s an emergency op as your appendix might burst and off we went to remove my appendix.

During this period, the hospital admin came to share with me the estimated cost, $18,000 and that Aviva has issued a letter of guarantee of $14,000. I believe this is the co-pay component kicking in. They mentioned that Medisave can be used to cover the difference up to $3,500, then the rest to be paid by cash.

Discharge

All went well during the operation, recovery was quick, the stay was great with the care from the nurses. During discharge, I was presented a bill of $17xxx of which I had to pay the difference of around $1,400 which I thought was ok only because my hospitalisation bill covered most of it.

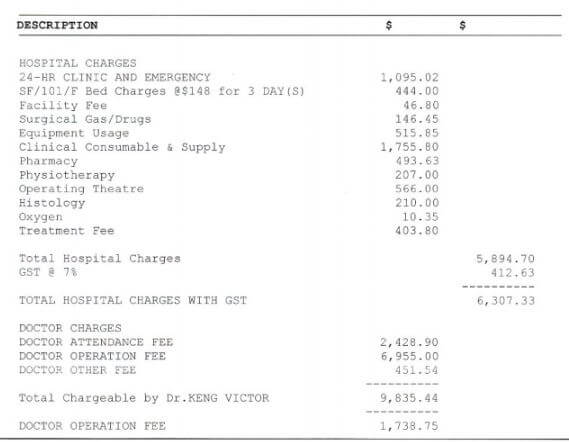

Here’s a breakdown of the bill

Have a look at the A&E cost, I spent about 2-3 hours there to get a dip.

Recovery

My road to recovery was a bit bumpy, I was given 2 weeks hospitalisation leave, went back to work on the 3rd week but towards the end of the week, I had a serious case of diarrhoea. I started having the runs for 9 days. During this time I went to 2 GPs and back to my surgeon which also incurred some post surgery medical bills.

Insurance Claims

Weeks after my little operation, I reached out to my insurance agent to fix my claims as I had company insurance and I had some post surgery claims to submit.

Here’s what he advised me to do

- Let your insurer tabulate the total cost and your entitlement. Sometimes you are entitled to loss of income if you are in hospital, based on your riders.

- Once you receive the final bill, reach out to your company insurer and fill up the required information to counter claim back, in my case Aviva will claim back from my company insurance and refund me anything that I paid out of pocket if the coverage is sufficient.

- Post operation period, if there are any complications, you can also claim that but it depends on the number of days your policy covers so you must check.

Key Lessons & Takeaways

After this episode, I’m thankful for my agent to convince me to get the integrated shield plan. It really helped me through this episode.

Apart from that, I believe we all should look at the following as well

- Know your policies, its coverage, entitlements and where you can use it. Both for personal and company insurance. This will help you make important choices on which hospital to go, what ward class to be in and most importantly a peace of mind.

- Be prudent, even if you are entitled to the best ward class, don’t go for the best, always leave room for complications. You don’t want to tap out the maximum claimable amount and leave no room for emergencies related to the op or hospitalisation event.

- Do some research on common alignment that your age bracket will experience. You want to make a list of specialists or doctors you can call on if you require them. I guess a lot of people like me just relied on the in house doctor recommendation but is the recommendation the best for you? You can’t prepare for all but do try to prepare.